Why I Am Buying Spire Global (SPIR) Stock in 2026

Posted on

Stock Research

Posted at

A Strategic Shift Positions Spire Global (SPIR)

Spire Global Inc. (NYSE: SPIR) is a leading global provider of space-based data, analytics, and space services. The company designs, builds, and operates a proprietary constellation of nanosatellites, known as LEMUR satellites, to collect real-time radio frequency (RF) data from low Earth orbit. This data powers subscription-based insights for maritime vessel tracking (prior to the 2025 divestiture), aviation monitoring, advanced weather forecasting, national security applications, and Space-as-a-Service solutions that let customers host their own payloads on Spire’s infrastructure.

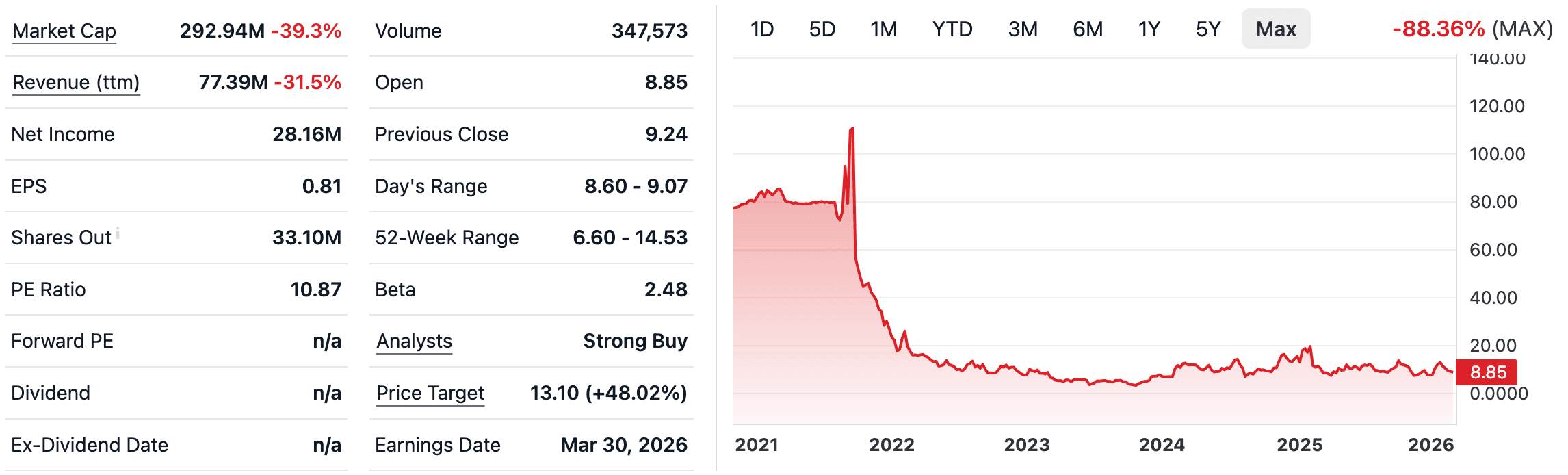

As we stand in early 2026, I am actively buying SPIR shares for my portfolio. After the strategic divestiture of the maritime business in April 2025, Spire has sharpened its focus on higher-margin segments like weather intelligence, aviation, government security contracts, and space services. With a robust backlog exceeding $200 million, multiple satellite launches already completed this year, and analyst price targets averaging around $13.70 (with highs to $19), the setup looks compelling for patient, growth-oriented investors.

This article breaks down exactly why SPIR represents one of the most attractive risk/reward opportunities in the small-cap space-tech sector right now. For more in-depth stock research, explore our dedicated stock analysis section or latest market commentary on the Stock Profit Club blog.

The space economy is projected to reach trillions of dollars in the coming decade, driven by demand for real-time Earth observation, climate intelligence, and secure data infrastructure. Spire Global sits at the intersection of these megatrends with a differentiated edge: its multi-purpose RF nanosatellites deliver persistent, global coverage that optical or imagery-focused peers simply cannot match at the same cost and frequency.

In 2025, Spire made a bold move by selling its maritime analytics unit. While this caused a temporary revenue dip (full-year 2025 guidance sits at $70.5–72.5 million), the divestiture removed a lower-margin segment and unlocked capital to double down on weather, aviation, national security, and Space-as-a-Service. Management now forecasts more than 30% revenue growth in 2026 for the remaining business, with approximately $70 million of the backlog converting to revenue this year alone.

I have followed space-tech names closely through our Stock Profit Club analysis platform, and Spire stands out for its execution on constellation expansion and contract momentum. Recent highlights include the successful January 2026 launch of nine satellites aboard SpaceX’s Twilight mission, including advanced hyperspectral microwave sounders for next-generation weather forecasting, plus ongoing deliveries for IoT and government customers.

With cash reserves near $97 million, minimal debt, and a clear roadmap to operating cash flow breakeven by the end of 2026, the company has the balance sheet runway to weather any short-term volatility while scaling. At a current market cap around $300 million and trading at roughly 3.5x trailing sales, SPIR offers asymmetric upside for investors who understand the long-term value of space-based intelligence.

Spire Global’s Core Technology

Spire’s constellation, one of the world’s largest commercial RF networks with well over 200 satellites launched to date and growing, captures signals that reveal ship movements, aircraft positions, atmospheric conditions, and even signals intelligence for defense applications. Unlike traditional Earth-imaging satellites that rely on cameras and revisit schedules, Spire’s nanosatellites provide near-continuous, all-weather, day-and-night coverage using passive RF listening.

This technology translates into four high-value solution areas post-maritime divestiture:

Weather Intelligence: AI-powered predictive analytics using space-based data for hyper-local forecasts, now enhanced by new hyperspectral microwave sensors launched in 2026. Customers include utilities, agriculture, and insurance firms seeking climate-risk insights.

Aviation: Real-time aircraft tracking and route optimization data that improves safety and efficiency for airlines and air-traffic management.

National Security & Government: RF data for domain awareness, spoofing/jamming detection, and policy applications. Recent wins include selection for the Missile Defense Agency’s SHIELD IDIQ contract and advisory board additions of high-profile national security figures in January 2026.

Space Services: “Space-as-a-Service” lets third parties (like Myriota for IoT) launch and operate payloads on Spire’s infrastructure, creating high-margin, recurring revenue with minimal additional capex for Spire.

Spire’s cost advantage is significant. Its 3U CubeSat design (roughly the size of a loaf of bread) keeps launch costs low via frequent SpaceX rideshares. The company has already demonstrated two-way optical inter-satellite laser links, slashing data latency by more than 10x and opening new real-time applications.

Compared to pure-play imagery peers like Planet Labs (PL) or BlackSky (BKSY), Spire’s RF focus provides complementary, often proprietary datasets that governments and enterprises pay recurring subscriptions to access. This sticky revenue model, combined with expanding constellation capacity, creates powerful operating leverage as fixed costs are spread across more data streams and customers.

For a deeper dive into comparable space-tech opportunities, see our recent coverage in the Stock Profit Club blog.

2026 Catalysts: Backlog Conversion, Launches, and Margin Expansion

The investment case for buying SPIR in 2026 rests on four near-term catalysts that are already visible.

First, backlog conversion. As of September 30, 2025, remaining performance obligations exceeded $200 million, with roughly $70 million earmarked for 2026 recognition. These are contracted, high-confidence revenues from multi-year government and commercial deals.

Second, constellation growth and new capabilities. Spire launched 39 satellites in 2025 alone and added nine more in January 2026, including advanced weather sensors. Each new satellite increases data collection capacity, improves revisit rates, and supports additional Space-as-a-Service missions. Management has signaled continued launches throughout 2026.

Third, commercial and government contract momentum. January 2026 announcements include a partnership with AiDASH to deliver space-powered weather intelligence for electric utility vegetation risk management, plus expansion of national security advisory capabilities. These wins validate Spire’s transition toward higher-value, defense-adjacent revenue.

Fourth, path to profitability. After years of heavy investment in the constellation, Spire targets adjusted EBITDA and operating cash flow breakeven no later than Q4 2026. Gross margins are already healthy on the core data business, and operating leverage will accelerate as revenue scales without proportional cost increases.

Taken together, these factors support management’s guidance for over 30% top-line growth in 2026, potentially reaching $90–95 million or more depending on execution. That would represent a sharp inflection from the transitional 2025 numbers and set the stage for sustained 25%+ compound growth thereafter as the space economy matures.

Attractive Entry Point in 2026

Let’s examine the numbers in detail. Here is a summary of key historical and forward-looking metrics:

Table 1: Spire Global Key Financial Metrics (in millions USD)

Metric | 2024 Actual | 2025 Guidance | 2026 Outlook (Est.) |

|---|---|---|---|

Revenue | 110.5 | 70.5–72.5 | 92–98 |

Gross Profit | 39.9 | ~28–30 | ~38–42 |

Operating Loss (GAAP) | (65.3) | ~(54) | Improving sharply |

Adjusted EBITDA | Negative | (42)–(41) | Approaching breakeven |

Cash Position (MRQ) | - | 96.8 | Strong runway |

Total Debt | - | ~12.5 | Minimal |

Note the dramatic improvement in the balance sheet: cash of approximately $97 million with very low debt provides more than two years of runway at current burn rates, even before growth kicks in.

Table 2: Valuation Multiples Comparison (as of February 2026)

Metric | SPIR Current | SPIR Forward (2026E) | Industry Avg (Space/Analytics) | Peer Example (PL/BKSY avg) |

|---|---|---|---|---|

Price/Sales | 3.8x | ~3.1x | 5–8x | 6.5x |

EV/Revenue | 2.9x | ~2.3x | 4–7x | 5.8x |

Price/Book | 2.3x | - | 3–5x | 4.1x |

Forward P/E | N/A (positive inflection) | ~6–8x (est.) | 15–25x | 18x |

Spire trades at a clear discount to both historical averages and direct peers on sales and enterprise value metrics. With analysts maintaining an average price target of $13.70 (implying ~55% upside from ~$8.85 levels) and one firm recently raising its target to $19, the street sees meaningful re-rating potential as 2026 results materialize.

For a simple DCF illustration (conservative assumptions: 2026 revenue $95M growing at 25% for five years, then 15% terminal, 35% gross margins expanding to 55%, 12% WACC):

Table 3: Simplified DCF Valuation Model

Year | Revenue | EBITDA Margin | Free Cash Flow (est.) | Discounted Value |

|---|---|---|---|---|

2026 | 95 | 5% | (10) | - |

2027 | 119 | 15% | 8 | 7.1 |

2028 | 149 | 25% | 22 | 17.5 |

2029 | 186 | 32% | 38 | 27.0 |

2030 | 233 | 38% | 55 | 35.0 |

Terminal | - | - | - | 280 (at 15x) |

Total Enterprise Value | - | - | - | ~$420M+ |

Per Share (diluted) | - | - | - | ~$12.50–14.00 |

This back-of-the-envelope model (using conservative growth and margin ramps) already supports the current analyst targets and suggests SPIR remains undervalued at today’s price.

Risks, Mitigation Strategies, and My Strategic Takeaway

No investment is without risk, particularly in the capital-intensive space sector. Here is a clear risk assessment:

Table 4: Key Risks and Mitigation for SPIR Investors in 2026

Risk | Likelihood | Potential Impact | Mitigation / Offset |

|---|---|---|---|

Execution delays on launches or contracts | Medium | Moderate | Proven track record of 39+ launches in 2025, diversified launch providers |

Government budget uncertainty | Medium | High | Growing commercial revenue mix, multi-year IDIQ contracts |

Increased competition in Earth observation | Low-Medium | Moderate | Unique RF dataset differentiation, patent-protected tech |

Dilution from equity raises | Low | Low-Moderate | Strong cash position reduces near-term need |

Macro slowdown affecting customer budgets | Medium | Moderate | Defensive nature of weather/security data demand |

Overall, risks feel manageable given Spire’s cash cushion, contracted backlog, and visible momentum. The biggest “risk” may actually be missing the re-rating as the market begins pricing in 2026–2027 profitability.

My Strategic Investor Takeaway I am buying SPIR in 2026 because the company has completed its strategic repositioning, the growth engine is now fully visible, and the valuation still embeds skepticism from the 2025 transition year. With a fully funded constellation expansion, sticky subscription revenue, and exposure to multiple secular tailwinds (climate intelligence, national security, commercial space infrastructure), Spire Global offers the rare combination of high growth, improving margins, and a discounted entry point.

For investors comfortable with small-cap volatility and a 2–4 year horizon, SPIR can deliver 2–3x returns as the market assigns a more appropriate multiple to its recurring revenue stream and path to positive cash flow. This is exactly the type of asymmetric opportunity we highlight regularly at Stock Profit Club.

Ready to dig deeper into SPIR or other space-tech names? Head to the Stock Profit Club homepage for our latest updates, portfolio ideas, and full stock analysis library. Join our community of serious retail and professional investors uncovering the next wave of growth opportunities.