Investing vs Trading: Which Strategy Truly Builds Long-Term Wealth?

Posted on

Start Investing

Posted at

Introduction, The Great Divide in the Markets

Few debates in personal finance are as persistent, or as consequential, as investing vs trading. Both activities take place in the same markets, involve the same securities, and ultimately pursue the same objective: turning capital into more capital. Yet they represent two fundamentally different philosophies about how markets work and how money is made.

At Stock Profit Club, we believe that the single most important decision any market participant makes is not which stock to buy, but which strategy to operate under. Choosing between investing and trading shapes every subsequent decision: your time horizon, your risk tolerance, your tax position, your psychological resilience requirements, and ultimately, your results.

This guide offers a comprehensive, authoritative breakdown of both approaches, backed by data and designed to give you the clarity you need to act with conviction.

Investing is the practice of allocating capital to financial assets, typically equities, bonds, or funds, with the expectation of generating returns over a multi-year or multi-decade time horizon. It relies on the underlying growth of businesses and the compounding of returns over time. Trading, by contrast, is the active buying and selling of financial instruments over short time frames, ranging from seconds to weeks, with the goal of capitalising on price fluctuations rather than business fundamentals.

Neither approach is inherently superior. However, the data suggests that for the overwhelming majority of market participants, understanding the structural differences between them is the difference between building wealth and eroding it.

Core Differences, A Side-by-Side Framework

To evaluate investing vs trading objectively, we must examine each dimension where they diverge: time horizon, methodology, capital requirements, tax treatment, psychological demands, and historical performance outcomes.

Time Horizon and Holding Period

The most fundamental distinction between investors and traders is time. An investor in a company like Apple or Microsoft in 2010 held through corrections, recessions, and geopolitical shocks, and generated compounding returns that dwarfed any single year's volatility. A trader operating in those same markets would have been forced to react to every fluctuation, generating transaction costs, tax events, and emotional pressure at each turn.

Buffett's famous aphorism, that his favourite holding period is "forever," encapsulates the investor's mindset. Traders, by contrast, must be right repeatedly, often dozens of times per week.

Table 1 — Investing vs Trading: Comprehensive Comparison Framework

Dimension | Investing | Trading |

|---|---|---|

Time Horizon | 1 year to decades | Seconds to weeks |

Primary Methodology | Fundamental analysis (earnings, moats, valuation) | Technical analysis (price action, volume, patterns) |

Decision Frequency | Low (weeks to months between decisions) | High (multiple decisions per session) |

Capital Requirement (typical) | $1,000 and above, scalable | $25,000 minimum for pattern day traders (US) |

Transaction Costs | Low, minimal portfolio turnover | High, frequent commissions and spreads |

Tax Treatment (US) | Long-term capital gains (0%, 15%, 20%) | Short-term capital gains (ordinary income rate, up to 37%) |

Primary Risk | Business deterioration, market drawdowns | Leverage, volatility, execution errors |

Psychological Demand | Moderate, patience and conviction required | Very High, rapid decision-making under pressure |

Income Type | Capital appreciation, dividends | Realised P&L from price movement |

Scalability | High, large capital compounds efficiently | Limited, market impact increases with size |

Methodology: Fundamentals vs Technicals

Investors conduct due diligence on the businesses behind the tickers. They analyse revenue growth trajectories, profit margins, return on invested capital, competitive moats, and management quality. The goal is to identify companies priced below their intrinsic value, then hold while the market recognises that value.

Traders largely discard fundamental analysis in favour of technical signals: moving averages, Relative Strength Index readings, support and resistance levels, volume patterns, and momentum indicators. Their thesis is that price action itself contains all relevant information, and that patterns repeat with enough statistical regularity to generate edge.

The Investor's Toolkit

Discounted Cash Flow (DCF) modelling

Price-to-Earnings and EV/EBITDA analysis

Balance sheet and debt structure review

Competitive moat assessment

Management track record evaluation

Dividend sustainability analysis

The Trader's Toolkit

Candlestick and chart pattern analysis

Moving averages (50 MA, 200 MA, EMA)

Volume profile and order flow

Relative Strength Index (RSI)

MACD and momentum oscillators

Level 2 quotes and options flow

Performance Data, What the Evidence Actually Shows

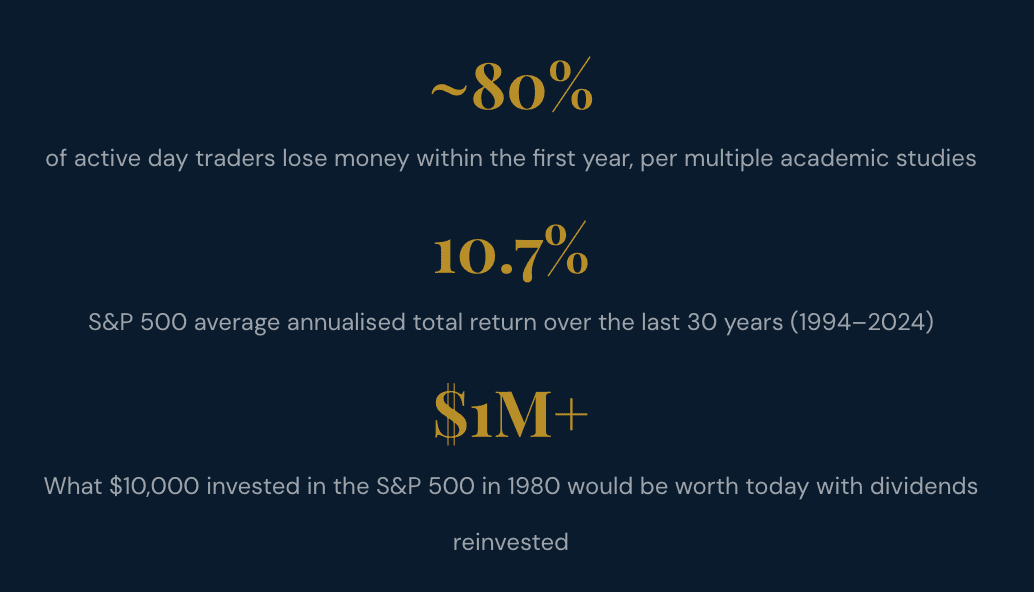

The empirical record on investing vs trading outcomes is more lopsided than most market participants expect. The data is not ambiguous: the structural advantages of long-term investing are substantial, and the odds against successful active trading are severe.

The Compounding Advantage for Investors

Albert Einstein reportedly described compound interest as the "eighth wonder of the world." Whether or not he said it, the mathematics are undeniable. A long-term investor who captures market returns with low costs and minimal tax drag has a structural advantage that is nearly impossible for an active trader to overcome consistently.

The following hypothetical illustrates the core dynamic, assuming a 10% annualised return for the investor and an 8% net return for the trader after costs, taxes, and the performance drag of losing years. Explore more strategies at Stock Profit Club.

Table 2 — Compounding Projection: $25,000 Starting Capital

Year | Long-Term Investor (10% p.a.) | Active Trader (8% net p.a.) | Advantage to Investor |

|---|---|---|---|

Year 1 | $27,500 | $27,000 | +$500 |

Year 5 | $40,263 | $36,733 | +$3,530 |

Year 10 | $64,844 | $53,973 | +$10,871 |

Year 20 | $168,187 | $116,524 | +$51,663 |

Year 30 | $436,235 | $251,566 | +$184,669 |

A 2% difference in annual net return, compounded over 30 years, produces a gap of nearly $185,000 on a $25,000 starting capital. For larger portfolios, the difference is generational.

When Trading Generates Superior Returns

It is intellectually dishonest to dismiss trading entirely. A minority of skilled traders, typically those with institutional-grade data access, sophisticated execution infrastructure, and robust risk management systems, do generate consistent alpha. Certain market environments, specifically high-volatility regimes, trending macro environments, or during earnings seasons, create genuine short-term opportunities.

"In the short run, the market is a voting machine. In the long run, it is a weighing machine."

Benjamin Graham, The Intelligent Investor

The critical distinction is between traders who approach the activity with professional rigour, a defined edge, disciplined position sizing, and systematic risk controls, and those who trade on intuition, tips, or the thrill of activity. The former can succeed. The latter statistically cannot, over time.

Risk Analysis, Understanding What You Are Actually Taking On

Every financial decision is a risk decision. The question is never whether to accept risk, but which risks you accept, at what price, and with what capacity to absorb the consequences. The risk profiles of investing and trading are structurally different, and confusing them is one of the most expensive mistakes a market participant can make.

Risk Profile Comparison

Table 3 — Risk and Reward Profile: Investing vs Trading

Risk Factor | Severity for Investor | Severity for Trader | Notes |

|---|---|---|---|

Market Drawdown Risk | Moderate | High | Traders may face margin calls during drawdowns |

Leverage Risk | Low (typically none) | Very High | Many traders use 2:1 to 10:1 or higher leverage |

Behavioural Risk | Moderate | Very High | FOMO, overtrading, and revenge trading are common |

Execution Risk | Low | High | Slippage, latency, and broker errors matter acutely |

Concentration Risk | Moderate | Moderate | Both strategies benefit from diversification |

Tax Drag Risk | Low | High | Frequent realised gains taxed at ordinary income rates |

Information Asymmetry | Low (long-term fundamentals are public) | High | Institutions have superior data and execution speed |

Capital Permanence Risk | Low | High | A single leveraged loss can wipe out a trading account |

The Behavioural Dimension

Risk is not purely financial. It is also psychological. Research in behavioural finance consistently demonstrates that human beings are poorly equipped for the demands that active trading places on them. Loss aversion causes traders to hold losing positions too long. Overconfidence leads to excessive position sizing. The dopamine response to winning trades creates compulsive re-entry even when the edge is absent.

Trading Behavioural Risks

Overtrading, revenge trading after losses, FOMO-driven entries, failure to honour stop-loss levels, and position-size escalation during drawdowns. These behaviours are statistically normal and financially devastating.

Investor Behavioural Advantages

Fewer decision points reduce error frequency. Long time horizons allow recoveries from volatility. Dividend reinvestment automates compounding. Lower cognitive load reduces decision fatigue and emotional interference.

For investors, the primary behavioural risk is panic-selling during market corrections, which locks in temporary losses and removes the capital needed to benefit from the subsequent recovery. The remedy is position sizing aligned to one's true risk tolerance, plus a pre-defined investment policy statement that removes emotion from decision-making during drawdowns.

Visit Stock Profit Club for in-depth guides on managing investment psychology and building a rules-based portfolio strategy.

Conclusion and Strategic Takeaway

The investing vs trading debate is ultimately a question of fit, not superiority. The right approach depends on your financial goals, available capital, time commitment, psychological temperament, and tax situation. However, the structural evidence does lean heavily in one direction for most people.

Long-term investing offers compounding returns, tax efficiency, scalability, and a forgiving error tolerance. It does not require real-time attention or the ability to outperform sophisticated institutional competitors on a daily basis. It does require patience, conviction, and the discipline to stay invested through volatility.

Active trading can generate outsized returns for a disciplined minority. It requires deep technical expertise, institutional-quality risk management, significant starting capital, and the psychological resilience to operate under continuous pressure. For most retail participants, the structural headwinds including transaction costs, tax drag, and information asymmetry are extremely difficult to overcome consistently.

A hybrid approach, maintaining a core long-term portfolio while allocating a defined, capped percentage of capital to shorter-term tactical positions, can offer a disciplined middle path for those with the skills and appetite for more active market participation.

Strategic Investor Takeaway

Before deciding between investing and trading, define your investment objectives, time horizon, and maximum tolerable drawdown. Build a core long-term portfolio using evidence-based principles, then add tactical exposure only if you have a demonstrable, tested edge and the risk management infrastructure to protect capital. If in doubt, the long game has consistently won.